48 / 87

48 / 87

April 2018

48

Fresh Water Boats For Sale

What You Can Do About

Rising Insurance Rates

Your Insurance

with

Cathy Karas

T

he industry trend for many types of personal insurance

is that rates are on the rise. I don’t know why this comes

at a surprise to many consumers since all you have to do

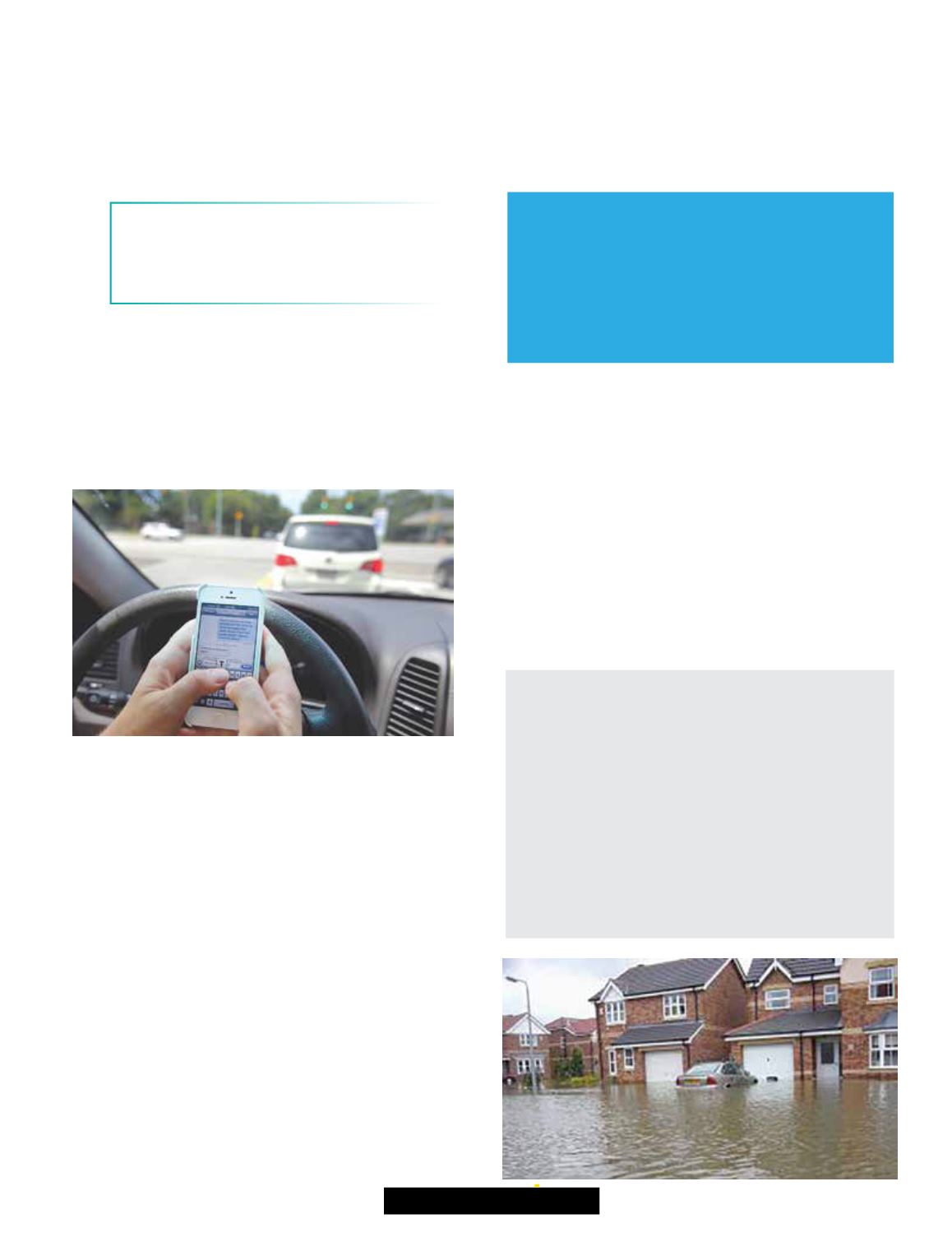

is turn on the TV or radio or read the newspaper to hear of

the volume of vehicle accidents involving distracted driving

while texting, talking on a phone or changing controls on the

dashboard, or wildfires, floods, or snow and rain damaging

homes. There are some proactive measures you can take

to reduce your costs that I will discuss later in my article,

but let’s first understand the nature of what insurance is and

the role the insurance companies play. Basically the idea

of insurance is to “spread the risk” among a segment of the

population and having the rates reflect an “average” cost for

this group where the insurance company will have enough

money to pay for losses that group will probably experience in

the upcoming year, make a profit, but not raise their rates so

high as to lose customers. Actuaries determine the chance

of a loss for a projected year, based on past history of prior

years for certain groups and come up with a premium. These

actuaries look at prior year’s experience for certain areas,

drivers, vehicles, home, boats, etc and base the rates on past

experience. There are many factors considered to determine

a rate. If the company paid out more than they collected in

premium for a certain population group, then the rate basis

was too low and they increase it, anticipating the claims

activity will be similar in the year upcoming. The reverse is

also true, where companies often take rate decreases, based

on favorable loss experience. For example after Storm

Sandy, many insurance companies either increased their

rates substantially for any properties with a coastal exposure

or chose to withdraw from issuing policies for those areas

altogether. After several years, some companies are now

accepting some business in the areas where they declined

it before or reduced their rates when other companies

re- entered the market place. Keep in mind insurance

companies are not charity organizations but companies

in business to make money. They have expenses as all

other business have such as payroll, insurance, rent, taxes

and other related expenses, as all businesses would .

Insurance companies are also required by the Insurance

Departments for each state to maintain a certain amount of

“reserve” to pay claims from.

Here are 3 common types of personal insurance and

rating factors that can affect your premium:

AUTO

Where you live (more congested

areas usually mean more traffic and more

accidents)

• Types of vehicles you own

• Your driving records and ages

• Limits of liability and deductibles if you

have comprehensive or comprehensive and

collision coverages

• Number of years you are with the

same company

and Why It’s

Happening