50 / 87

50 / 87

February - March 2018

50

Find Us On Facebook at Boating On The Hudson

Your Insurance

with

Cathy Karas.

DOES YOUR HOMEOWNERS

POLICY RESPOND TO

POTENTIAL WINTER CLAIMS?

I

don’t know about you,

but enough already with the

cold temperatures! By the time you read this issue, your thoughts

may be turning to the upcoming boating season as March is

around the corner. But first we must deal with the harshest

months of the year. Our main concern regarding our homes

is the potential for fire loss. However there are many other

components to a homeowners policy that may cover situations

you are unaware of. Let’s look at some potential winter claims

that could occur and see of your policy will respond with a claim

payment. For this article I am referring to the most typical New

York homeowners insurance policy form also known as “Special

Form”. Your policy form may either be more enhanced or more

basic, but these causes los loss will give you a general idea of

what to expect should you experience any of these situations.

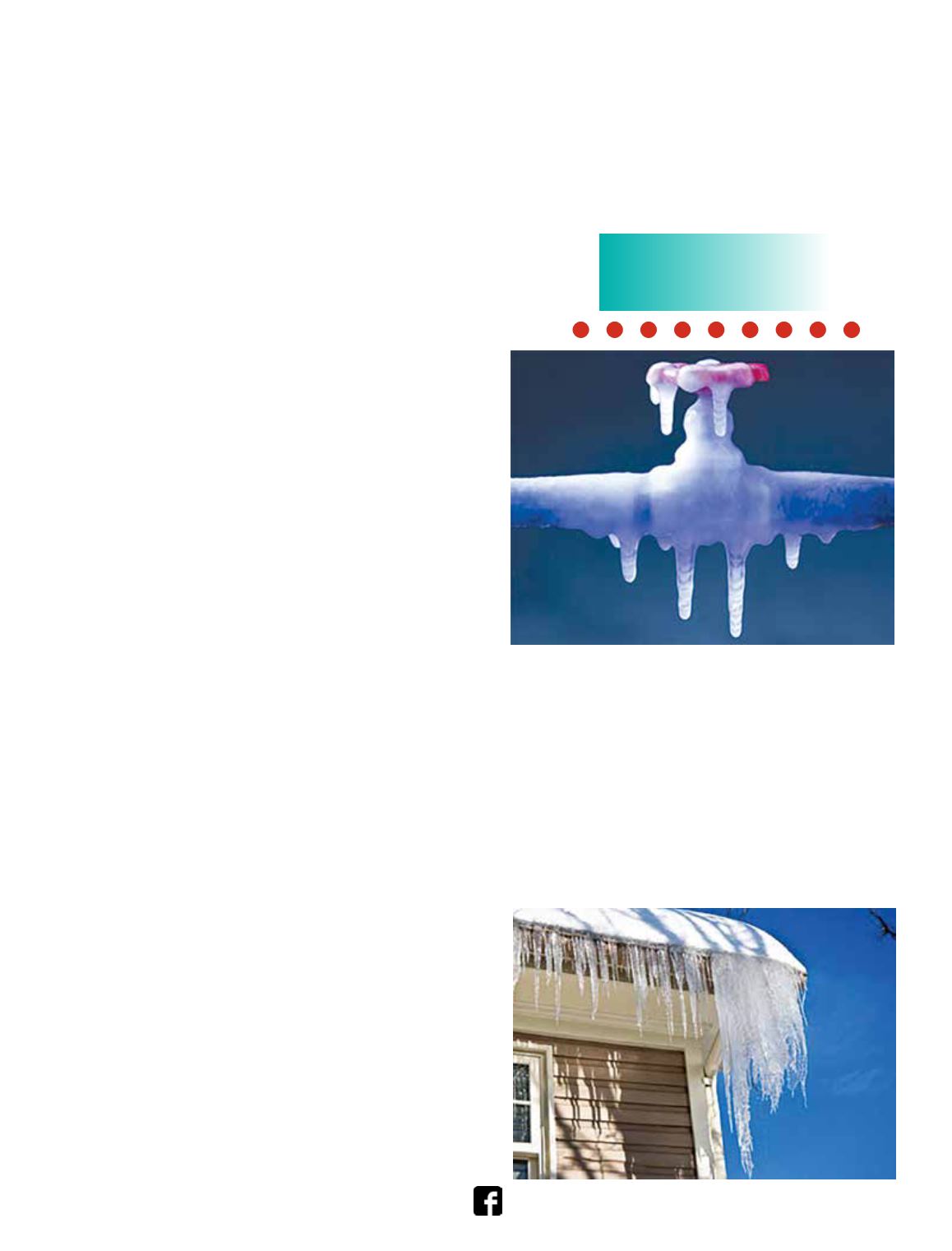

FROZEN PIPES -

Hopefully you have done all you can

to avoid this by leaving water trickling through faucets where

pipes are connecting through an exterior wall. In your kitchen

it is also a good idea to leave the cabinet doors open under

your sink to allow warmer air in the room circulate around the

pipes and warm the area, if there is an exterior wall there. (Be

sure to remove cleaning products children and pets could get

into.) If you do have a frozen pipe that bursts and causes water

damage, your homeowners policy should pay for the resulting

damage the water causes, but not the repair of the pipe itself.

If there is too much water for you to safely clean up yourself,

and/or can’t get it to stop, call a restoration company to do

this professionally. The homeowners policy conditions require

you protect property from further damage, so most likely the

insurance company will pick up this charge, if your claim is

covered. Take photos before you do anything if possible, and

if you do call a restoration service or plumbing contractor, save

receipts for any necessary immediate repairs. Water entering

your home at ground level is generally not covered such as

what originates outside relating pipes under the street not on

your property.

FIRE -

If you have a supplementary heating source such

as a wood or pellet stove or are using your fireplace, be sure

a contractor as cleaned or checked it recently. Be sure it is

safely vented. Do not dispose of embers that have any heat

and certainly not anywhere near your home, garage or any

other structures or vehicles. Make sure your flue is open when

using a fireplace and closed when not in use to avoid loss

of heat through the chimney. Don’t leave unattended or on

while you are sleeping. Even the newer “safe” electric heaters

could experience an electrical malfunction or tip over, causing

a fire. Be in the room when using these supplemental heating

sources. Regarding your stove, this is not a safe supplemental

heating source. Even if electric, using the burners or oven to

warm your kitchen is not safe.

ICE DAM -

When it gets warmer and you have an

accumulation of ice and or snow on your roof and your

gutters, the water that results from the melting can back

up through the gutters and or shingles causing damage to

the interior ceilings, walls and maybe even your personal

property inside. These claims can be extensive, so any

preventative measures you or a contractor can perform

to clear the roof and gutters can minimize this type of

damage. I had this situation at my own home and the

water traveled throughout the entire living room ceiling,

causing water to leak through several areas.

LOSS OF POWER -

Frozen pipes can result from